All Categories

Featured

[/image][=video]

[/video]

Holding money in an IUL repaired account being attributed interest can frequently be far better than holding the money on deposit at a bank.: You've always imagined opening your own bakery. You can obtain from your IUL plan to cover the preliminary costs of renting a space, acquiring tools, and hiring team.

Credit report cards can supply a flexible way to obtain money for very short-term periods. Obtaining cash on a debt card is normally really costly with yearly portion rates of interest (APR) commonly reaching 20% to 30% or even more a year.

The tax therapy of policy loans can differ substantially relying on your country of home and the specific terms of your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy finances are usually tax-free, offering a substantial benefit. Nonetheless, in other jurisdictions, there may be tax implications to take into consideration, such as prospective taxes on the finance.

Term life insurance policy only offers a survivor benefit, without any kind of cash money worth build-up. This implies there's no cash money worth to obtain against. This short article is authored by Carlton Crabbe, President of Capital permanently, a professional in giving indexed universal life insurance accounts. The details offered in this short article is for academic and informational objectives just and must not be construed as financial or investment suggestions.

How To Become Your Own Bank

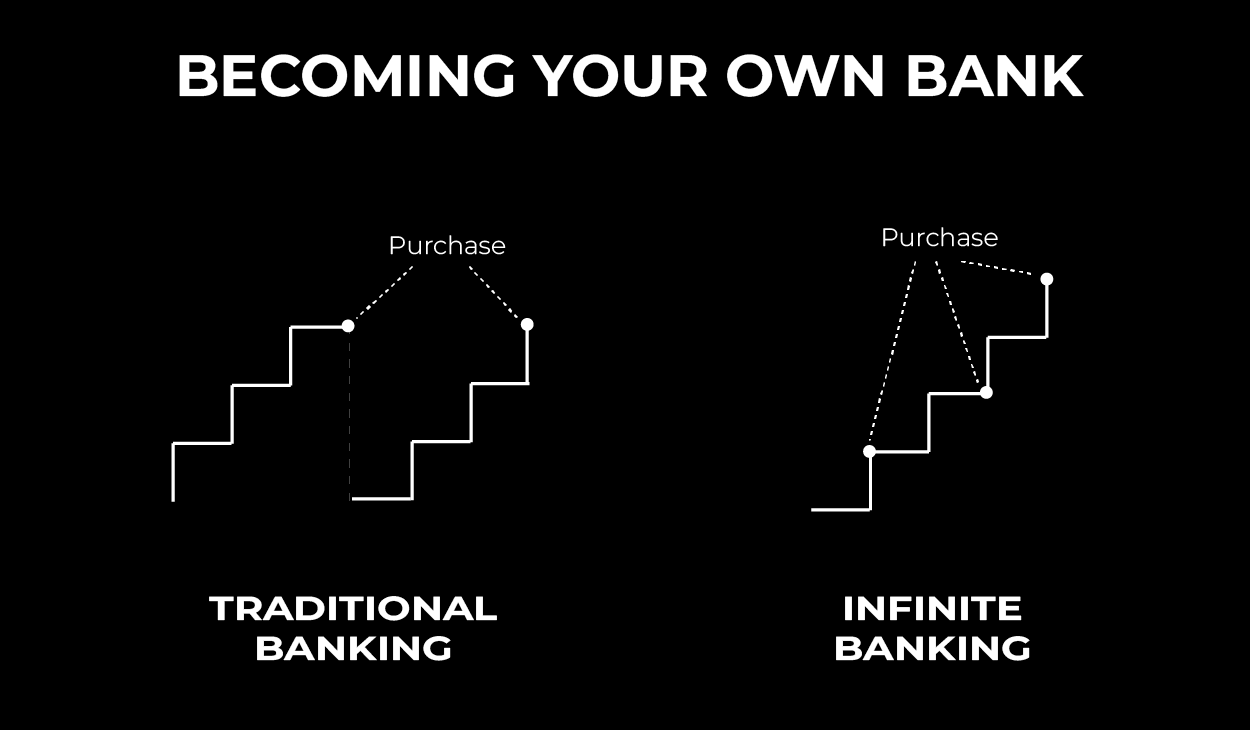

Imagine entering the monetary world where you're the master of your domain name, crafting your own course with the skill of a skilled banker but without the constraints of imposing establishments. Invite to the world of Infinite Financial, where your economic destiny is not just a possibility yet a concrete fact.

Uncategorized Feb 25, 2025 Money is just one of those points we all handle, however the majority of us were never truly educated exactly how to utilize it to our benefit. We're informed to conserve, spend, and budget plan, yet the system we run in is created to maintain us based on financial institutions, regularly paying passion and charges simply to access our own cash.

She's a professional in Infinite Financial, a strategy that helps you repossess control of your funds and build actual, long lasting riches. And trust fund methis isn't some "money bro" magic technique. It's a real technique that rich families like the Rockefellers and Rothschilds have been using for generations. Let's get involved in it.

Currently, before you roll your eyes and think, Wait, life insurance? This is a high-cash-value plan that permits you to: Shop your money in a place where it expands tax-free Borrow versus it whenever you require to make financial investments or major purchases Gain uninterrupted substance rate of interest on your cash, even when you obtain versus it Think about how a bank works.

With Infinite Financial, you come to be the financial institution, earning that interest rather of paying it. For many of us, cash moves out of our hands the second we get it.

How To Be My Own Bank

The insurer does not need to get "repaid," since it will simply be deducted from what gets distributed to your recipients upon your expiry day, as Hannah so euphemistically called it. You pay on your own back with interest, just like a financial institution wouldbut now, you're the one benefiting. Allow that sink in.

It's about redirecting your money in a manner that constructs wide range as opposed to draining it. If you remain in actual estateor desire to bethis strategy is a found diamond. Let's claim you want to get an investment property. Rather of mosting likely to a financial institution for a car loan, you obtain from your very own plan for the deposit.

You use the loan to purchase your home. Rental earnings or benefit from the offer repay your policy instead of a financial institution. This implies you're building equity in your policy AND in realty at the same time. That's what Hannah calls double-dippingand it's precisely just how the wealthy maintain growing their cash.

How To Be Your Own Banker

Allow's remove a few up. Below's the thingthis isn't a financial investment; it's a cost savings strategy. Investments involve risk; this doesn't. Your money is ensured to expand no issue what the stock exchange is doing. Maybe, but this isn't about either-or. You can still buy genuine estate, supplies, or businessesbut you run your cash via your policy first, so it maintains expanding while you spend.

See to it you work with an Infinite Financial Concept (IBC) professional that comprehends just how to establish it up appropriately. This approach is a complete frame of mind change. We have actually been educated to believe that banks hold the power, however the truth isyou can take that power back. Hannah's family has been using this strategy since 2008, and they currently have more than 38 policies funding real estate, investments, and their family's monetary legacy.

Becoming Your Own Banker is a text for a ten-hour course of guideline about the power of dividend-paying entire life insurance policy. The market has actually focused on the death advantage high qualities of the contract and has neglected to properly describe the funding capabilities that it provides for the plan owners.

This publication demonstrates that your requirement for money, during your life time, is much higher than your need for defense. Fix for this demand via this tool and you will finish up with more life insurance policy than the firms will certainly provide on you. Most everyone recognizes with the fact that one can obtain from a whole life policy, yet because of how little costs they pay, there is minimal accessibility to cash to fund major items required throughout a life time.

Truly, all this publication contributes to the equation is range.

{kind=link}

Latest Posts

How To Be Your Own Bank In Just 4 Steps

Infinite Banking Examples

Infinite Banking